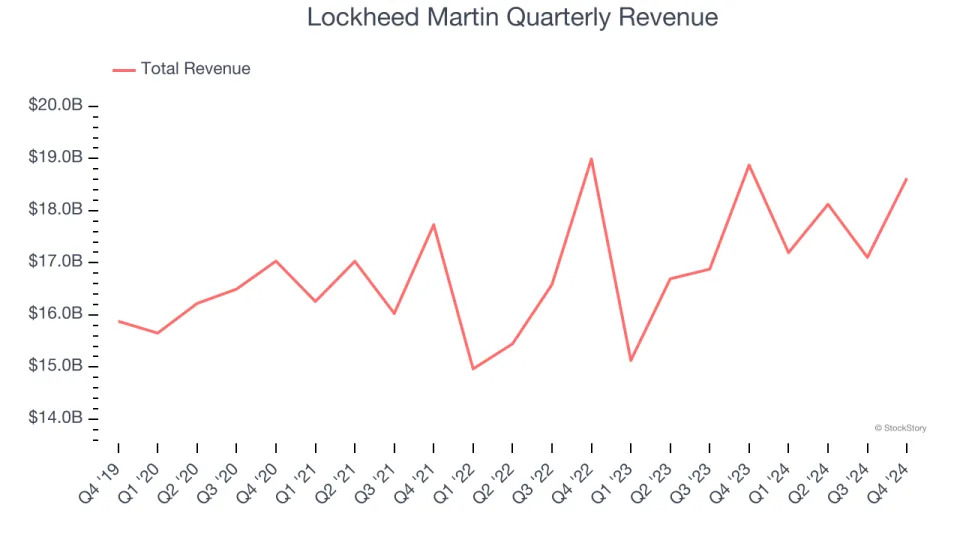

Security and Aerospace company Lockheed Martin (NYSE:LMT) fell short of the market’s revenue expectations in Q4 CY2024, with sales falling 1.3% year on year to $18.62 billion. On the other hand, the company’s outlook for the full year was close to analysts’ estimates with revenue guided to $74.25 billion at the midpoint. Its GAAP profit of $2.22 per share was 66.3% below analysts’ consensus estimates.

Is now the time to buy Lockheed Martin? Find out in our full research report .

"2024 was another successful and productive year for Lockheed Martin. Our 5% sales growth and record year-end backlog of $176 billion demonstrate the enduring global demand for our advanced defense technology and systems," said Jim Taiclet, Lockheed Martin's Chairman, President and CEO.

Headquartered in Maryland, Famous for the F-35 aircraft, Lockheed Martin (NYSE:LMT) specializes in defense, space, homeland security, and information technology products.

Defense contractors typically require technical expertise and government clearance. Companies in this sector can also enjoy long-term contracts with government bodies, leading to more predictable revenues. Combined, these factors create high barriers to entry and can lead to limited competition. Lately, geopolitical tensions–whether it be Russia’s invasion of Ukraine or China’s aggression towards Taiwan–highlight the need for defense spending. On the other hand, demand for these products can ebb and flow with defense budgets and even who is president, as different administrations can have vastly different ideas of how to allocate federal funds.

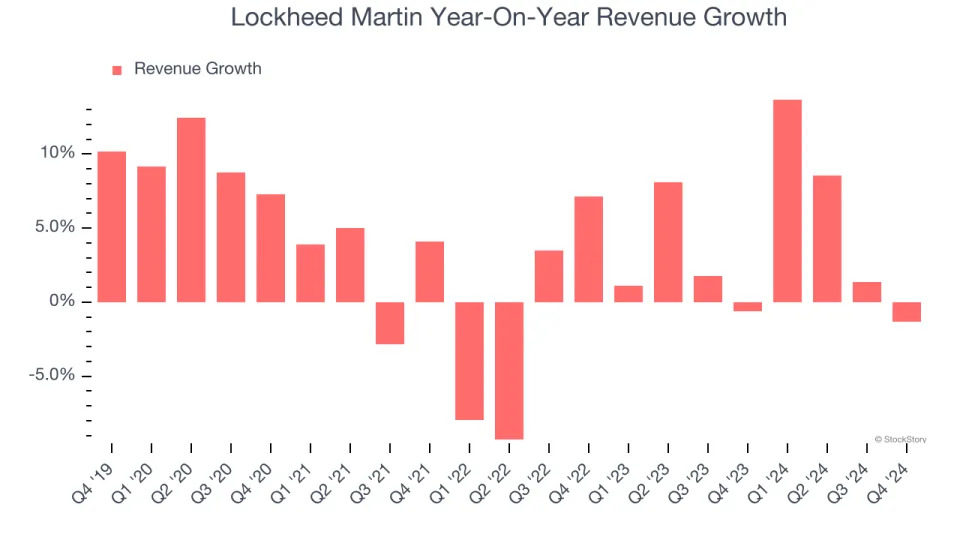

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Lockheed Martin grew its sales at a sluggish 3.5% compounded annual growth rate. This fell short of our benchmark for the industrials sector and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Lockheed Martin’s annualized revenue growth of 3.8% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

This quarter, Lockheed Martin missed Wall Street’s estimates and reported a rather uninspiring 1.3% year-on-year revenue decline, generating $18.62 billion of revenue.

Looking ahead, sell-side analysts expect revenue to grow 3.9% over the next 12 months, similar to its two-year rate. This projection is underwhelming and indicates its newer products and services will not lead to better top-line performance yet.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link .

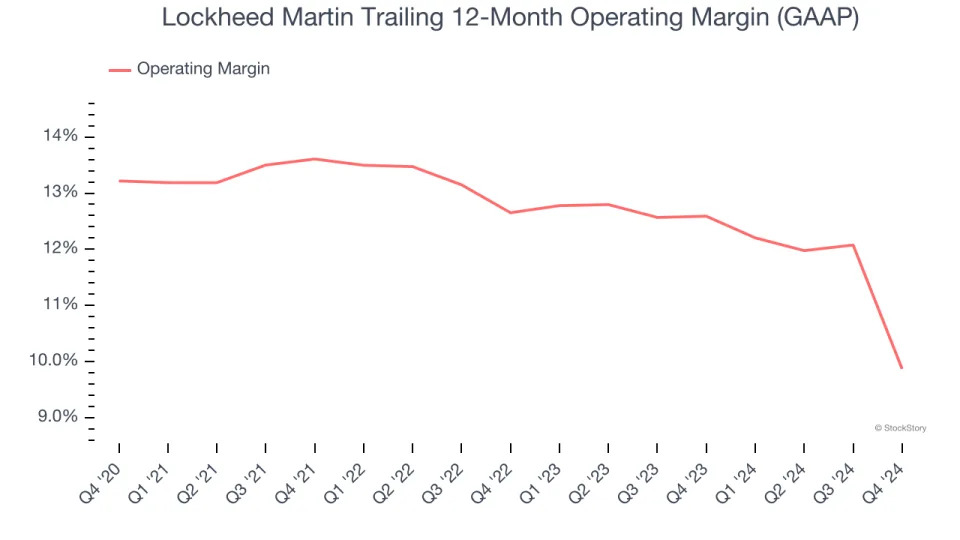

Lockheed Martin has been an optimally-run company over the last five years. It was one of the more profitable businesses in the industrials sector, boasting an average operating margin of 12.4%.

Looking at the trend in its profitability, Lockheed Martin’s operating margin decreased by 3.3 percentage points over the last five years. Even though its historical margin is high, shareholders will want to see Lockheed Martin become more profitable in the future.

In Q4, Lockheed Martin generated an operating profit margin of 3.7%, down 8.4 percentage points year on year. This contraction shows it was recently less efficient because its expenses increased relative to its revenue.

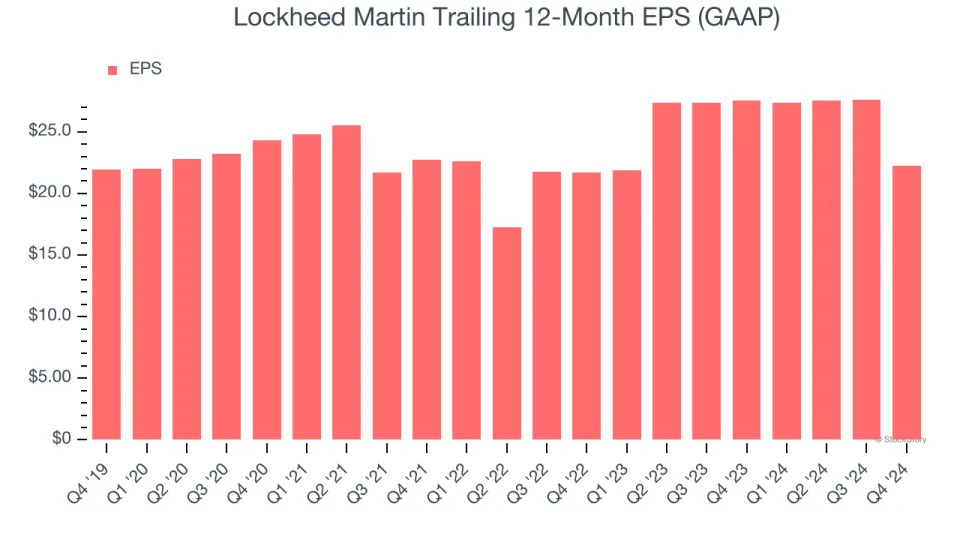

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Lockheed Martin’s flat EPS over the last five years was below its 3.5% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

We can take a deeper look into Lockheed Martin’s earnings to better understand the drivers of its performance. As we mentioned earlier, Lockheed Martin’s operating margin declined by 3.3 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Lockheed Martin, its two-year annual EPS growth of 1.3% is similar to its five-year trend, implying stable earnings.

In Q4, Lockheed Martin reported EPS at $2.22, down from $7.58 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Lockheed Martin’s full-year EPS of $22.26 to grow 25.5%.

We struggled to find many resounding positives in these results as its full-year EPS guidance missed significantly. This quarter's EPS also fell short of Wall Street’s estimates because the company recorded a $1.3 billion loss in its Missiles and Fire Control (MFC) business segment. Overall, these results could have been better. The stock traded down 3.6% to $486.02 immediately after reporting.

The latest quarter from Lockheed Martin’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. We think that the latest quarter is just one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free .