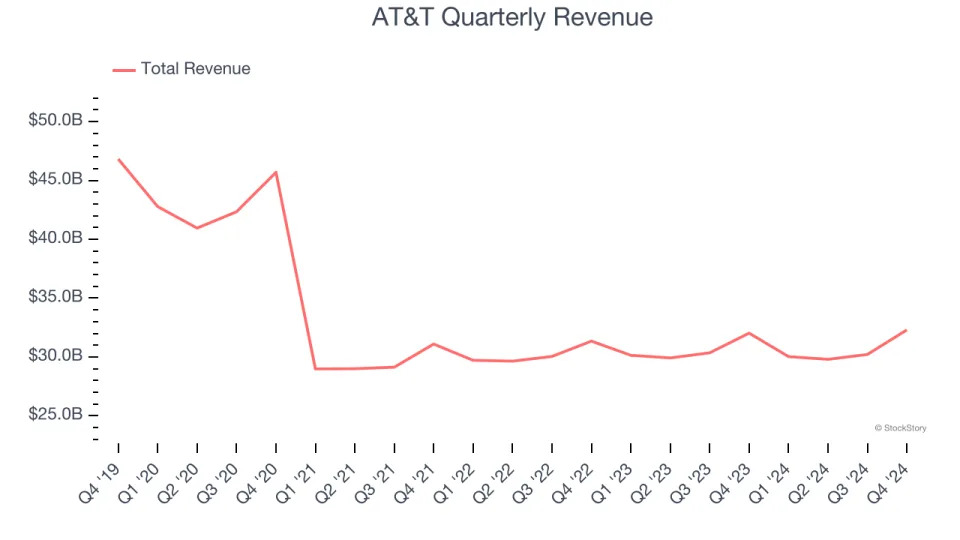

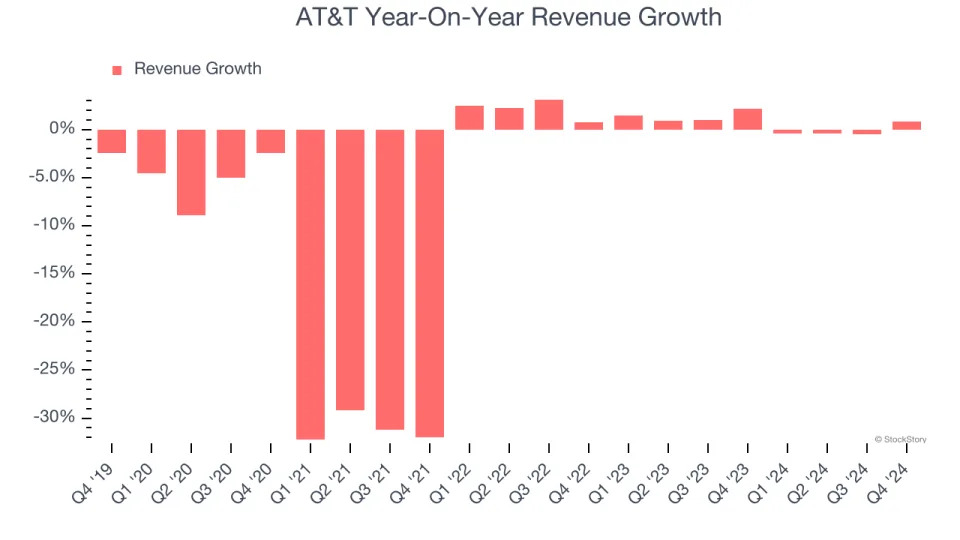

Telecommunications conglomerate AT&T (NYSE:T) reported revenue ahead of Wall Street’s expectations in Q4 CY2024, but sales were flat year on year at $32.3 billion. Its non-GAAP profit of $0.54 per share was 6.1% above analysts’ consensus estimates.

Is now the time to buy AT&T? Find out in our full research report .

Founded by Alexander Graham Bell, AT&T (NYSE:T) is a multinational telecomm conglomerate providing a range of communications and internet services.

The massive physical footprints of cell phone towers, fiber in the ground, or satellites in space make it challenging for companies in this industry to adjust to shifting consumer habits. Over the last decade-plus, consumers have ‘cut the cord’ to their landlines and traditional cable subscriptions in favor of wireless communications and streaming video. These trends do mean that more households need cell phone plans and high-speed internet. Companies that successfully serve customers can enjoy high retention rates and pricing power since the options for mobile and internet connectivity in any geography are usually limited.

A company’s long-term performance is an indicator of its overall quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for years. Over the last five years, AT&T’s demand was weak and its revenue declined by 7.6% per year. This fell short of our benchmarks and is a sign of poor business quality.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. AT&T’s revenue over the last two years was flat, sugggesting its demand was weak but stabilized after its initial drop in sales.

We can dig further into the company’s revenue dynamics by analyzing its most important segment, Mobility. Over the last two years, AT&T’s Mobility revenue (wireless plans) averaged 2.1% year-on-year growth. This segment has outperformed its total sales during the same period, lifting the company’s performance.

This quarter, AT&T’s $32.3 billion of revenue was flat year on year but beat Wall Street’s estimates by 1.1%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. This projection doesn't excite us and implies its newer products and services will not accelerate its top-line performance yet.

Today’s young investors likely haven’t read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next .

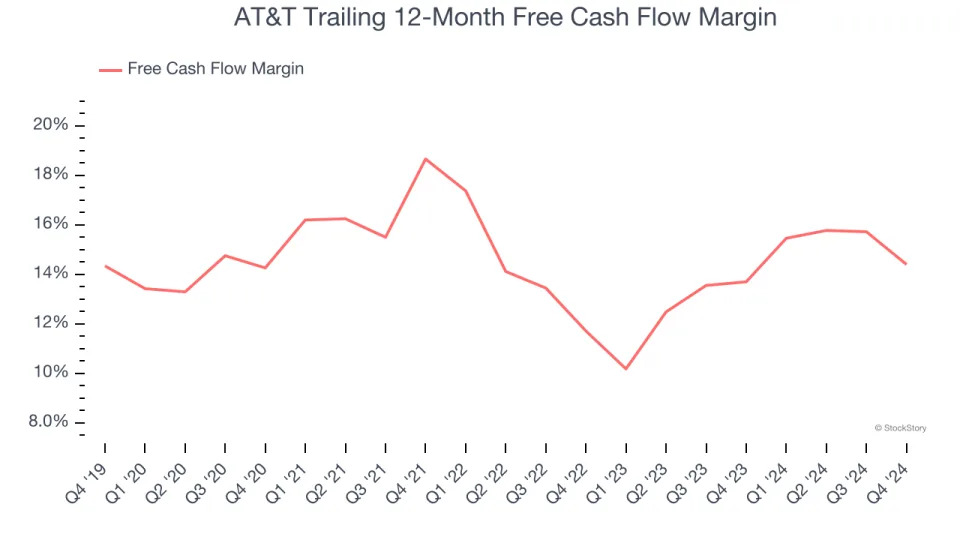

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

AT&T has shown impressive cash profitability, giving it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 14% over the last two years, better than the broader consumer discretionary sector.

AT&T’s free cash flow clocked in at $4.8 billion in Q4, equivalent to a 14.9% margin. The company’s cash profitability regressed as it was 5 percentage points lower than in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

Over the next year, analysts predict AT&T’s cash conversion will slightly improve. Their consensus estimates imply its free cash flow margin of 14.4% for the last 12 months will increase to 15.6%, giving it more flexibility for investments, share buybacks, and dividends.

It was encouraging to see AT&T beat analysts’ EPS expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. Overall, this quarter had some key positives. The stock traded up 1.4% to $23.02 immediately after reporting.

Is AT&T an attractive investment opportunity at the current price? We think that the latest quarter is just one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free .