Adobe

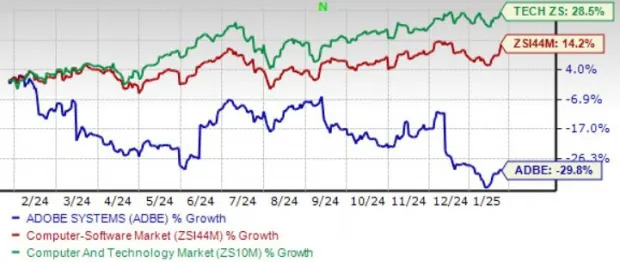

ADBE shares have declined 29.8% in the trailing 12-month period, underperforming the broader Zacks Computer and Technology sector’s return of 28.5% and the Zacks Computer Software industry’s appreciation of 14.2%.

ADBE’s 2025 prospects are suffering from increasing competition in the Generative AI (GenAI) space from the likes of

Microsoft

MSFT-backed Open AI, as well as a lack of monetization of its AI solutions.

For fiscal 2025, Digital Media Annual Recurring Revenue is now expected to grow roughly 11%. Digital Media segment revenues are expected between $17.25 billion and 17.40 billion, suggesting 9% growth at the mid-point over fiscal 2024. The guidance reflects lower benefits from pricing and more focus on AI user engagement instead of monetization.

Adobe expects total revenues between $23.30 billion and $23.55 billion ($21.51 billion in fiscal 2024). Unfavorable forex and continued move to subscriptions from perpetual offerings are expected to negatively impact revenues by $200 million.

Fiscal 2025 non-GAAP earnings are now expected between $20.20 and $20.50 ($18.42 per share in fiscal 2024).

For fiscal 2025, the Zacks Consensus Estimate for earnings is pegged at $20.39 per share, down 0.7% over the past 60 days. The figure indicates 10.69% growth from that reported in fiscal 2024.

ADBE’s earnings beat the Zacks Consensus Estimate in the trailing four quarters, the average surprise being 2.55%.

Adobe Inc. price-consensus-chart | Adobe Inc. Quote

Find the latest EPS estimates and surprises on Zacks Earnings Calendar

.

The Zacks Consensus Estimate for fiscal 2025 revenues is pegged at $23.45 billion, suggesting 9.04% growth from that reported in fiscal 2024.

Adobe stock is not so cheap, as the Value Score of D suggests a stretched valuation at this moment.

In terms of the forward 12-month price/sales, ADBE is trading at 8X, higher than the sector’s 7.17X.

Adobe’s prospects are expected to benefit from strong demand for its creative products. Its Creative Cloud, Document Cloud and Adobe Experience Cloud products have been driving top-line growth.

New AI releases, including Express, Acrobat AI Assistant, Firefly Services, DX premium tiers and GenStudio for Performance Marketing, have expanded the portfolio of products. These are expected to drive Adobe’s market share and monetization in the near future.

Adobe expanded its GenAI portfolio with the launch of Firefly Image Model 3, enhancements to vector models, richer design models and the all-new Firefly video model. The deep integration of these models into Adobe’s tools, like Lightroom, Photoshop, Premiere, InDesign and Express, has improved the experience of creative professionals globally. Firefly generations now have crossed 16 billion cumulative generations.

Strong Adobe Express adoption by businesses is noteworthy. The increasing number of integrations into leading social, productivity and collaboration apps like ChatGPT,

Alphabet

GOOGL division Google, Slack, Wix, Box, Hubspot and Webflow significantly increased Adobe Express’ customer reach.

Adobe’s Document Cloud AI Assistant is now available in Acrobat across desktop, web and mobile and integrated into Chrome, Microsoft Teams and Edge extensions. Adobe GenStudio, which integrates Express, Firefly, Workfront, Experience Manager, Customer Journey Analytics and Journey Optimizer, is riding on strong adoption in the content supply chain for enterprises.

Adobe’s expanded partnership with

Amazon

AMZN makes the Adobe Experience Platform available on Amazon Web Services. Partnerships with Google’s Campaign Manager 360, Meta Platforms, Microsoft Advertising, Snap and TikTok are key catalysts.

Adobe is winning clients in both the Creative Cloud and Document Cloud segments.

Alphabet, American Express, Coca-Cola, Johnson & Johnson, LVMH, Procter & Gamble, T-Mobile and the U.S. Department of Defense were major additions to the Creative Cloud clientele in the fiscal fourth quarter.

Abbott Laboratories, BWI GmbH, Defense Information Systems Agency, Kaiser Permanente, Novo Nordisk, Truist, U.S. Cellular and the U.S. Department of State were major additions to the Document Cloud clientele.

Adobe’s deepening GenAI focus and innovative GenAI-powered portfolio are key catalysts. Hence, investors who already own the stock may expect the company's growth prospects to be rewarding over the long term.

However, intensifying competition from the likes of OpenAI is concerning. While Adobe’s video model will be widely available in early 2025, OpenAI’s video-generating Sora is available to users already paying for ChatGPT. Lack of monetization is a headwind.

Stretched valuation makes the stock unattractive for value-oriented investors.

ADBE currently has a Zacks Rank #3 (Hold), which implies that investors should wait for a more favorable time to accumulate the stock.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Amazon.com, Inc. (AMZN) : Free Stock Analysis Report

Microsoft Corporation (MSFT) : Free Stock Analysis Report

Adobe Inc. (ADBE) : Free Stock Analysis Report

Alphabet Inc. (GOOGL) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research