PayPal

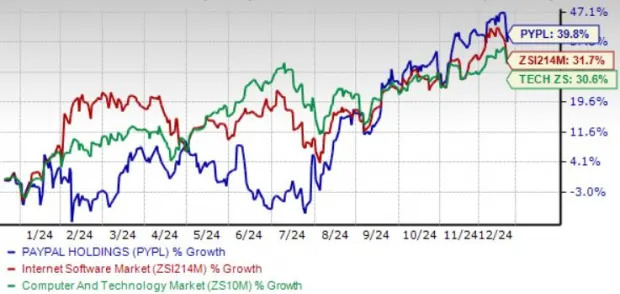

PYPL shares have returned 39.8%, outperforming the Zacks Computer and Technology sector’s return of 30.6% and the Zacks Internet Software industry’s appreciation of 31.7%.

PYPL’s portfolio strength has been helping it maintain deep and trusted relationships with merchants and consumers. Its two-sided platform helps develop direct financial relationships with customers and merchants.

Expanding clientele benefited total payment volume, which increased 9% year over year, both on a spot-rate basis and forex-neutral basis, to $422.641 billion in the third quarter of 2024.

PayPal saw year-over-year growth of 1% in total active accounts to 432 million, while payment transactions per active account were 61.4 million, up 9% year over year.

Transaction margin of $3.7 billion grew more than 8% on a reported basis and more than 6% ex-interest on customer balances, driven by higher interest income, branded checkout, Venmo, Braintree, and tech-led risk/loss improvements.

PYPL saw a 15% to 20% increase in Buy Now, Pay Later use in the reported quarter.

PYPL is one of the cheaper stocks in the industry, as suggested by the Value Score of B.

PYPL stock is trading at a significant discount with a forward 12-month P/E of 17.77X compared with the industry’s 35.24X.

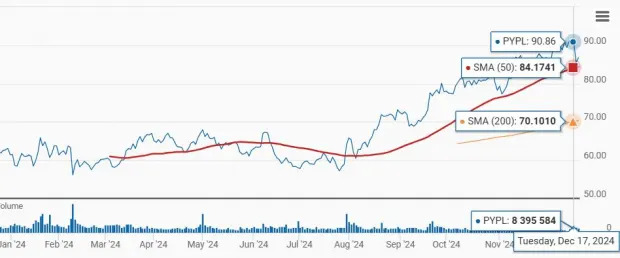

PayPal shares are trading above the 50-day and 200-day moving averages, indicating a bullish trend.

A strong portfolio is a growth driver for PYPL. The unveiling of Fastlane, which enhances the guest checkout experience by allowing users to complete their purchase in one click, remains noteworthy. Since its August launch, more than 1,000 merchants have been using Fastlane to provide a seamless experience to their customers and drive increased conversion.

Currently, it is available in the United States. Fastlane is based on the company's decades of payment expertise to innovate and accelerate the guest checkout experience.

The launch of PayPal Complete Payments in new geographies, including China and Hong Kong, expands its footprint among small and medium-sized businesses (SMBs). PayPal expects to expand its service to more markets in 2025.

PayPal’s expanding partner base, including Fiserv, Adyen,

Amazon

AMZN, Global Payments and

Shopify

SHOP, is driving prospects. The rich partner base is expected to help increase the adoption of PYPL’s Fastlane.

PayPal is now an additional processor for Shopify Payments in the United States. Its branded checkout solutions are now integrated into Shopify Payments. This creates a single and unified experience for business owners to drive operational efficiency.

PayPal’s partnership with Amazon now brings PayPal Checkout to SMBs offering Buy with Prime. In 2025, it will give Prime members the option to link their Amazon and PayPal accounts so that consumers can receive Prime shipping benefits when they use PayPal while shopping with Buy with Prime.

Its collaboration with Apple and Google to integrate the Venmo debit card with Apple Pay and Google Pay has been a noteworthy development.

PayPal is a top payment method for advertisers and consumers globally across

Meta Platforms

’ META family of apps. Creators and developers are using Hyperwallet. META also uses Braintree for credit card processing.

For 2024, PayPal now anticipates non-GAAP earnings growth in the high teens (up from previous guidance of low to mid-teens growth) over 2023.

The Zacks Consensus Estimate for earnings is pegged at $4.57 per share, up 2.93% over the past 60 days, suggesting a 10.39% decline over 2023’s reported figure.

The consensus mark for revenues is currently pegged at $31.68 billion, indicating 6.4% growth over the 2023 reported figure.

PayPal expects transaction margin dollar growth in the mid-single-digits for 2024.

For the fourth quarter of 2024, PayPal expects low-single-digit revenue growth. Non-GAAP earnings are expected to exhibit a low to mid-single-digit decrease on a year-over-year basis.

The Zacks Consensus Estimate for revenues is pegged at $8.24 billion, indicating 2.66% year-over-year growth.

The Zacks Consensus Estimate for earnings is pegged at $1.10 per share, indicating a 25.68% decline from the figure reported in the year-ago quarter. However, the earnings figure has been steady over the past 60 days.

PYPL’s earnings beat the Zacks Consensus Estimate in the trailing four quarters, the average surprise being 15.14%.

Find the latest EPS estimates and surprises on Zacks Earnings Calendar

.

PayPal’s robust portfolio, expanding partner base and cheap valuation are key drivers that make the stock attractive to long-term investors. Hence, investors who already own the stock may expect the company's growth prospects to be rewarding over the long term.

However, PYPL expects lower Braintree volume and revenue growth in the fourth quarter and through 2025. Higher non-transaction operating expenses due to marketing spending are expected to hurt profits in the fourth quarter of 2024. Non-transaction operating expenses for 2024 is now expected to increase in the low-single digit range. The trend is likely to continue in 2025.

PayPal currently has a Zacks Rank #3 (Hold), suggesting that it may be wise to wait for a more favorable entry point in the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Amazon.com, Inc. (AMZN) : Free Stock Analysis Report

PayPal Holdings, Inc. (PYPL) : Free Stock Analysis Report

Shopify Inc. (SHOP) : Free Stock Analysis Report

Meta Platforms, Inc. (META) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research